December 18, 2018

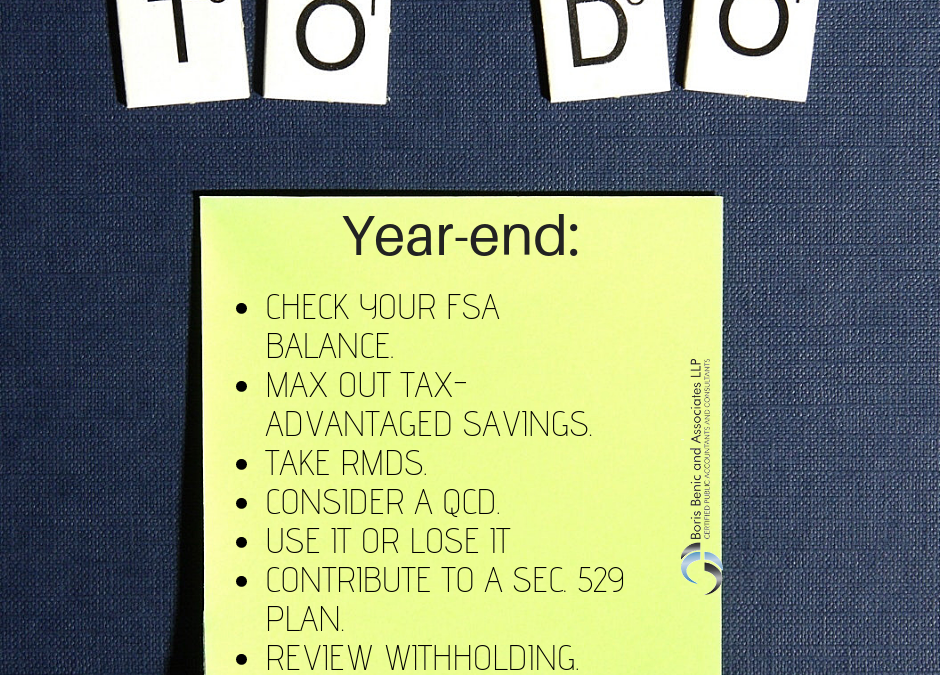

With the dawn of 2019 on the near horizon, here’s a quick list of tax and financial to-dos you should address before 2018 ends:

- Check your FSA balance. If you have a Flexible Spending Account (FSA) for health care expenses, you need to incur qualifying expenses by December 31 to use up these funds or you’ll potentially lose them. (Some plans allow you to carry over up to $500 to the following year or give you a 2½-month grace period to incur qualifying expenses.) Use expiring FSA funds to pay for eyeglasses, dental work or eligible drugs or health products.

- Max out tax-advantaged savings. Reduce your 2018 income by contributing to traditional IRAs, employer-sponsored retirement plans or Health Savings Accounts to the extent you’re eligible. (Certain vehicles, including traditional and SEP IRAs, allow you to deduct contributions on your 2018 return if they’re made by April 15, 2019.)

- Take RMDs. If you’ve reached age 70½, you generally must take required minimum distributions (RMDs) from IRAs or qualified employer-sponsored retirement plans before the end of the year to avoid a 50% penalty. If you turned 70½ this year, you have until April 1, 2019, to take your first RMD. But keep in mind that, if you defer your first distribution, you’ll have to take two next year.

- Consider a QCD. If you’re 70½ or older and charitably inclined, a qualified charitable distribution (QCD) allows you to transfer up to $100,000 tax-free directly from your IRA to a qualified charity and to apply the amount toward your RMD. This is a big advantage if you wouldn’t otherwise qualify for a charitable deduction (because you don’t itemize, for example).

- Use it or lose it. Make the most of annual limits that don’t carry over from year to year, even if doing so won’t provide an income tax deduction. For example, if gift and estate taxes are a concern, make annual exclusion gifts up to $15,000 per recipient. If you have a Coverdell Education Savings Account, contribute the maximum amount you’re allowed.

- Contribute to a Sec. 529 plan. Sec. 529 prepaid tuition or college savings plans aren’t subject to federal annual contribution limits and don’t provide a federal income tax deduction. But contributions may entitle you to a state income tax deduction (depending on your state and plan).

- Review withholding. The IRS cautions that people with more complex tax situations face the possibility of having their income taxes underwithheld due to changes under the Tax Cuts and Jobs Act. Use its withholding calculator (available at irs.gov) to review your situation. If it looks like you could face underpayment penalties, increase withholdings from your or your spouse’s wages for the remainder of the year. (Withholdings, unlike estimated tax payments, are treated as if they were paid evenly over the year.)

For assistance with these and other year-end planning ideas, please contact us.

© 2018 Thomson Reuters/Tax & Accounting